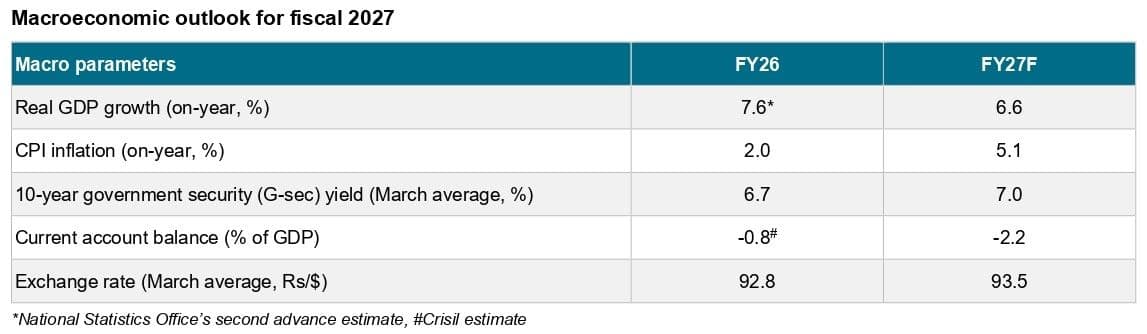

New Delhi: India’s economic resilience is facing its sternest test since the pandemic as the prolonged closure of the Strait of Hormuz threatens to derail growth, fuel inflation and strain government finances. Considering this, Crisil has sharply revised its macroeconomic outlook for fiscal 2027, warning that the combined impact of elevated crude prices, supply-chain disruptions and climate-linked weather risks could drag India’s GDP growth down to 6.6% from 7.6% estimated for fiscal 2026. Inflation, meanwhile, is projected to more than double to 5.1%.

The warning comes at a time when global energy markets remain deeply unsettled despite diplomatic efforts to stabilise West Asia. Brent crude prices have stayed above $100 a barrel for weeks, with ripple effects spreading across freight, fertilisers, manufacturing inputs and financial markets. India, which imports the bulk of its crude requirements, is particularly vulnerable to sustained supply disruptions through the Strait of Hormuz, one of the world’s most critical oil transit routes.

In its report, Shock and Woe: Revising Our India Economic Outlook, Crisil Intelligence said the economic fallout from the conflict has already started materialising across sectors, forcing a downward revision in growth estimates and a steep upward revision in inflation projections.

“The Strait of Hormuz has been de facto shut for over two months, amplifying the global energy shock. This will take time to normalise because of the damage to oil and gas infrastructure in West Asia — even after the route reopens,” says the report. “Crisil Intelligence has revised its Brent crude price forecast to $90-95 per barrel for fiscal 2027 from $82-87. The shock extends beyond energy to freight and insurance costs, supply chains, and fertilisers, which have a multidimensional impact on the economy.”

The report said the prolonged disruption has created “the largest energy shock on record”, with oil and derivatives markets continuing to suffer supply losses equivalent to at least 10% of global supply. That has intensified concerns around imported inflation and industrial costs for emerging economies such as India.

Inflation Risks Rise

Crisil expects higher commodity prices and weaker global demand to weigh heavily on India’s manufacturing and export sectors over the next fiscal. Sectors dependent on imported raw materials are likely to face margin pressure as logistics costs and energy prices remain elevated.

“We expect real gross domestic product (GDP) growth to slow to 6.6% in fiscal 2027 from 7.6% in fiscal 2026 because of higher crude oil and other commodity prices, softer global growth amid the conflict and forecasts of a below-normal monsoon,” says the report. “Input cost pressures from the spike in crude oil and gas prices will weigh on growth. Global supply chain disruptions and the reduced availability of gas and other inputs will add to the pressure.”

The report flags exports as another major area of concern. Slowing growth in the US and Eurozone — which together account for around 37% of India’s goods exports — could significantly weaken external demand. Crisil noted that India’s exports to West Asia have already begun slowing sharply amid the conflict.

Compounding the pressure is the growing threat of an El Niño-driven weak monsoon. The India Meteorological Department’s forecast of rainfall at 92% of the long-period average has raised concerns over agricultural output and food inflation. According to the report, weaker kharif and rabi harvests could amplify inflationary pressures at a time when households are already grappling with elevated costs.

“We expect inflation based on the Consumer Price Index (CPI) to average 5.1% in fiscal 2027 from 2.0% in fiscal 2026, driven by a low-base effect and expectations of broadening price pressures across major segments,” says Crisil. “The West Asia conflict has disrupted supply chains and raised international freight and insurance costs. This, coupled with a depreciating rupee, will raise the cost of imported inputs.”

Crisil also warned that higher inflation could shrink the Reserve Bank of India’s monetary policy space, limiting the scope for growth-supportive rate actions. The benchmark 10-year government security yield is expected to rise to 7% by March 2027 as subsidy burdens increase and foreign capital flows remain volatile.

Resilience Under Pressure

The report projects India’s current account deficit to widen sharply to 2.2% of GDP in fiscal 2027 from an estimated 0.8% last fiscal, driven primarily by a swelling oil import bill. The rupee is also expected to remain under pressure, averaging 93.5 against the dollar by March 2027.

Crisil said the conflict could also hurt remittance inflows from West Asia, which accounted for 38% of India’s total remittances in fiscal 2024, according to RBI data. A prolonged slowdown in the region would therefore have implications beyond trade and energy.

At the same time, the report acknowledged that India still retains some buffers against the external shock. Strong corporate balance sheets, well-capitalised banks and continued government capital expenditure are expected to cushion the economy from a deeper slowdown. The Centre’s push on infrastructure spending and state-led cash transfer programmes could also support consumption demand.

“The West Asia conflict is a fresh reminder to build economic resilience to global shocks,” says the report. “Three imperatives can help India build economic resilience over the medium term.” It added that India must accelerate renewable energy adoption, strengthen food security and continue structural reforms to sustain long-term growth.