New Delhi: Central banks are making one of their biggest collective bets in decades, and it is on gold. As geopolitical tensions, trade disputes and fiscal risks mount, reserve managers are increasing bullion allocations at a pace that suggests the trend is no longer cyclical but structural. The implications extend beyond the precious metals market, pointing to a gradual reordering of the global financial system.

Official institutions have bought more than 1,000 tonnes of gold annually for four consecutive years, roughly double the average pace of the previous decade. With central banks now holding gold as a strategic hedge against uncertainty, the buying spree is expected to continue despite record prices.

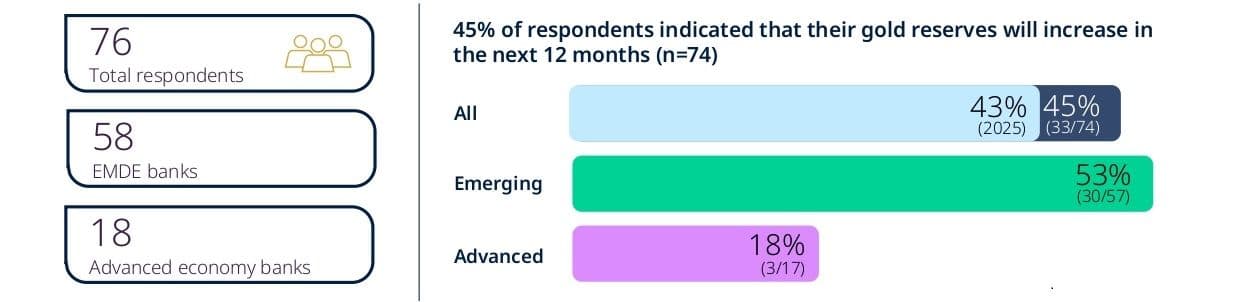

That conclusion comes from the World Gold Council’s Central Bank Gold Reserves Survey 2026, which polled 76 central banks between February and May, the highest participation since the study began. The survey found that 95% of respondents expect global central bank gold reserves to increase or remain stable over the next 12 months, while a record 89% believe total official gold holdings worldwide will rise. More significantly, 45% expect their own institutions to increase gold reserves over the coming year, the highest reading since the survey was launched.

The findings suggest that central banks are rewriting the rules of reserve management. For decades, foreign exchange portfolios were largely built around the US dollar and other major currencies. Today, gold is increasingly viewed as a core reserve asset capable of insulating national balance sheets from geopolitical and financial shocks.

One central banker explained the thinking behind the trend. “We expect the weight of gold in reserves to increase over this horizon as a main consequence of increased purchases by central banks to increase gold reserves, mainly of developing countries, in the context of increasing the level of diversification in the portfolio.”

Reserve diversification has emerged as the single biggest driver of planned gold purchases. Among central banks intending to buy more bullion, 31 out of 34 cited diversification policy as a key factor, followed by the need for stronger protection against inflation, market instability and exposure to the US dollar.

The trend is particularly pronounced among emerging market and developing economy (EMDE) central banks. Their reserve managers are significantly more likely than advanced economy peers to expand gold holdings, reflecting efforts to strengthen financial resilience in an increasingly fragmented global economy.

Dollar Faces Challenge

The resurgence of gold is closely linked to shifting attitudes towards the US dollar. While reserve managers continue to regard the greenback as the world’s dominant reserve currency, many expect its influence to gradually decline over the next five years.

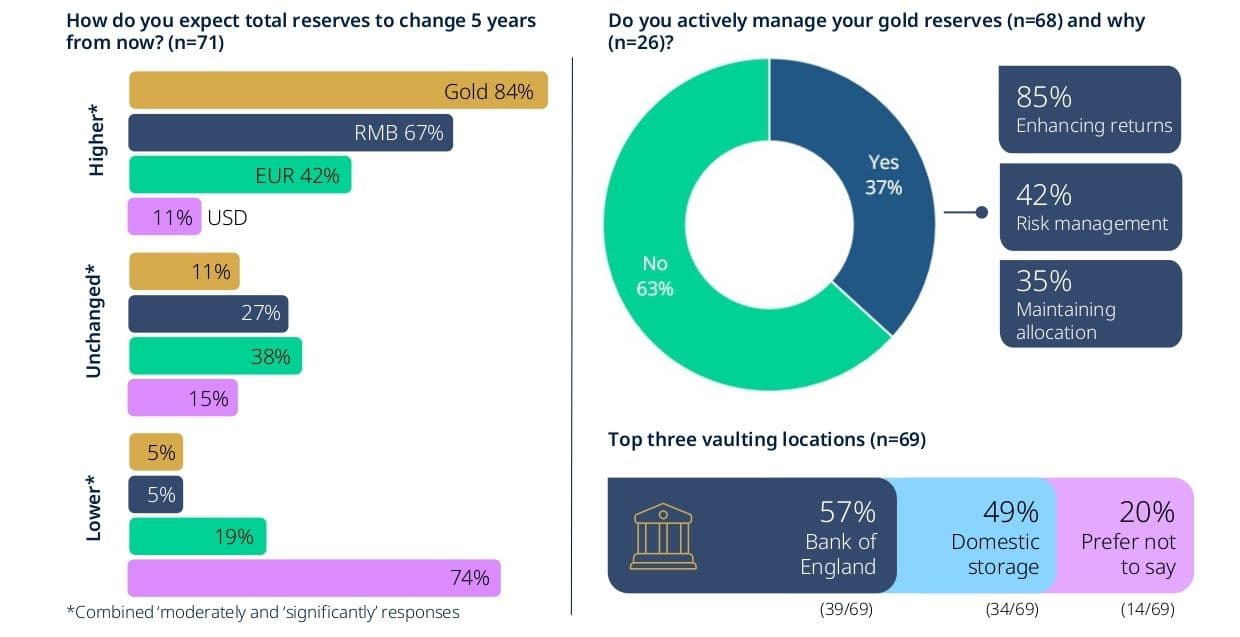

The survey shows that 74% of respondents expect the share of global reserves denominated in US dollars to fall over that period. Gold, by contrast, is expected to gain a larger role in reserve portfolios, with 84% anticipating an increase in its share of total reserves. Current reserve composition data show the US dollar accounting for 42% of global reserves, followed by gold at 26%, the euro at 15% and the Chinese renminbi at just 1%.

The shift should not be mistaken for a wholesale move away from the dollar. Central banks continue to value the liquidity, scale and depth of US financial markets. Instead, reserve managers are pursuing a strategy of diversification to reduce concentration risk.

One of the respondents noted, “Although interest in diversifying away from the US dollar has grown, the liquidity and depth of dollar-denominated assets remain far superior to those of other alternatives.”

Another offered a glimpse of the future reserve landscape. “In five years, USD will remain dominant though lower than the current. Gold and CNY and others may widen further in terms of allocations in the next five years.”

The broader macroeconomic backdrop reinforces that view. Interest rates remain the biggest concern for reserve managers, cited by 92% of respondents, while 88% identified geopolitical instability as a major risk and 79% pointed to inflation. EMDE central banks expressed even greater concern, with 95% highlighting geopolitical risks.

Trade tensions are becoming an increasingly important consideration. More than half of central banks planning to increase gold holdings cited rising risks from tariffs and trade conflicts, while many also flagged rising budget deficits in major economies and slowing growth across advanced markets.

One respondent summed up the changing investment landscape, saying, “Gold may benefit from increasing geopolitical and commercial tensions.”

The survey also points to concerns about future supply dynamics. “Buying patterns will increase as less and less gold mines are available to meet demand dynamics, another central banker observed:

Reserves Reimagined

The survey reveals that central bank gold strategies are becoming more sophisticated, extending beyond accumulation into active management, domestic sourcing and storage diversification.

About half of central banks planning to buy more gold intend to finance purchases through domestic gold acquisition programmes using local currencies. Around 38% expect to sell existing reserve assets to fund acquisitions, while 32% will use newly accumulated reserves.

The way central banks manage gold is also changing. Around 76% manage bullion separately from other reserve assets, underscoring its role as a strategic rather than tactical holding. About 37% actively manage gold reserves, with 85% of those seeking to enhance returns and 42% focusing on risk management, nearly double last year’s level.

Physical security remains a priority. The Bank of England continues to be the preferred international vaulting location, used by 57% of respondents, while domestic storage and overseas custody diversification are gaining traction. Nine % increased domestic storage over the past year and 10% diversified overseas storage arrangements.

Good Delivery bars remain the preferred form of physical ownership, and a growing number of central banks are upgrading holdings to meet international standards, improving liquidity and marketability.

The motivations for holding gold have become increasingly strategic. Around 90% of respondents identified its performance during crises as a key reason for ownership, while 84% highlighted its role as a long-term store of value and inflation hedge. More than 80% cited portfolio diversification, geopolitical risk protection and gold’s absence of default risk.

The survey also shows that central banks are looking beyond traditional reserve assets. While most have no immediate plans to increase exposure to equities, corporate bonds or alternative investments, gold continues to stand apart as the preferred strategic asset in an uncertain world.

One of the respondents perhaps best captured the significance of the current cycle. “Given the central bank gold purchases have exceeded the historical average over the past four years, with new central banks continuing to join the trend, it is possible that the share of gold reserves will increase in the current environment of uncertainty.”

The message from the world’s reserve managers is clear. Central banks are not abandoning the dollar, nor are they preparing for a return to a gold standard. Instead, they are building larger bullion buffers against sanctions risks, fiscal imbalances, geopolitical conflict and market volatility.

For the gold market, sustained official sector demand is likely to provide a powerful structural support. For investors, it reinforces gold's status as a safe-haven asset. For policymakers, it signals that the age of concentrated reserve holdings is giving way to a more diversified global monetary order, with gold reclaiming a central role in safeguarding national wealth.