New Delhi: India’s rural economy is undergoing a structural shift, one that’s quietly but decisively linking land ownership with financial empowerment. As formal property documentation expands across villages, access to institutional credit is widening, loan sizes are increasing, and households once excluded from formal finance are entering the banking system with new credibility.

The implications go beyond rural India. Policymakers are now weighing whether this model can be adapted to urban areas, where fragmented land records continue to constrain transparency, efficiency and investment.

The transformation underway stems from the recognition that unclear property rights have long acted as a brake on credit expansion. Without verifiable ownership, rural households could not leverage their most valuable asset — their homes. What the government’s SVAMITVA (Survey of Villages and Mapping with Improvised Technology in Village Areas)scheme has done is to bridge this gap by converting informal holdings into legally recognised, financeable assets.

The shift has altered both sides of the credit equation. Banks are now better equipped to verify collateral, while households, armed with property cards, are more inclined to approach formal institutions. This interplay between supply and demand is what gives the reform its momentum. It also reflects a deeper behavioural transition, where ownership is no longer merely a marker of social status but an entry point into formal economic participation.

“The Government of India’s introduction of the SVAMITVA scheme marks a landmark policy effort in rural property-rights reform. By seeking to provide formal recognition to residential abadi holdings that have long remained outside clear legal and financial records, the scheme lays foundation for stronger tenure security, better local governance and wider participation in formal credit markets,” states the working paper titled ‘Unlocking Rural Property Rights: Social Inclusion and Credit Expansion through SVAMITVA’, released by the Economic Advisory Council to the Prime Minister.

Mapping: Scale & Technology

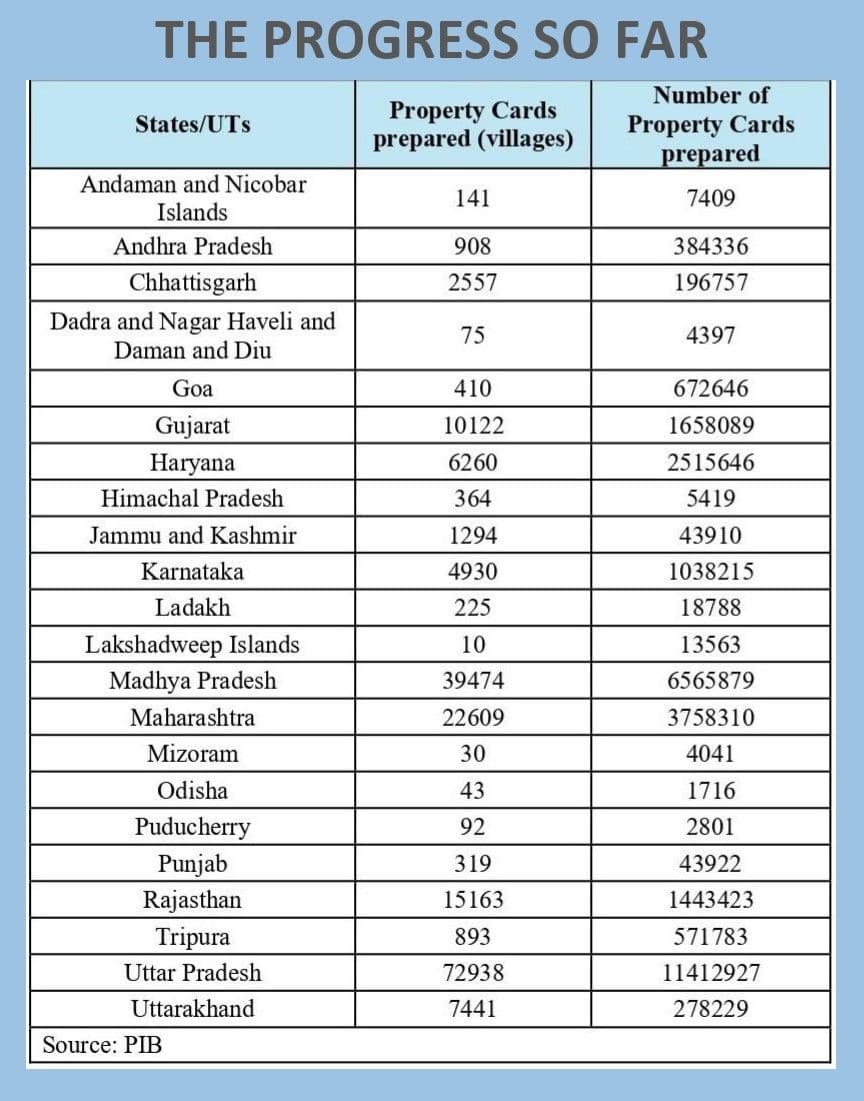

The impact of SVAMITVA is inseparable from its scale and technological backbone. Since its nationwide rollout in April 2021, the programme has moved rapidly, with around 3.06 crore property cards prepared across nearly 1.86 lakh villages by early 2026, highlight the report’s authors. This scale ensures that the reform is not confined to isolated beneficiaries but reshapes financial behaviour at the district level.

The technological architecture behind the scheme has been equally critical. Drone-based mapping, combined with GIS tools and ground verification, has enabled the creation of accurate, geo-referenced land records. These are then integrated into state systems and translated into legally recognised property cards, providing a level of clarity that was previously absent in rural abadi areas.

This clarity has institutional consequences. The scheme effectively redefines rural property from an informal possession into a documented, verifiable asset. In doing so, it reduces ambiguity for lenders and enhances the usability of land as collateral. The report underscores that such formalisation also lowers transaction and verification costs, making the credit appraisal process more efficient and predictable for financial institutions.

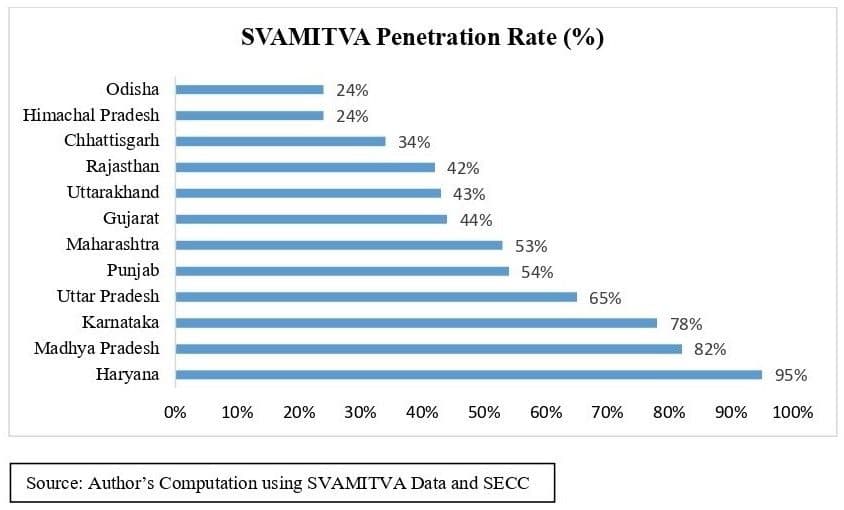

The scale of coverage reinforces this effect. With drone surveys completed in over 95% of notified villages and a penetration rate estimated at around 53% of rural households, SVAMITVA operates as a systemic intervention. Lending practices, verification norms, and borrower behaviour are all being reshaped simultaneously.

Importantly, the implementation journey is evolving. While the mapping phase is nearing saturation, the next stage involves resolving disputes, validating claims, and ensuring last-mile distribution of property cards. This shift from aerial mapping to ground-level adjudication highlights the administrative complexity of property reform and the need for sustained institutional capacity.

Beyond credit markets, the scheme is also strengthening governance frameworks. Digitised land records are enabling better tax assessment, improving local revenue mobilisation, and supporting more effective village-level planning. Gram panchayats, equipped with accurate spatial data, are better positioned to manage resources and design development interventions.

Formalisation & Credit Expansion

The most visible outcome of this institutional shift is the surge in formal credit. Districts where SVAMITVA has been implemented have recorded a 23% increase in sanctioned loan amounts, a finding derived from rigorous empirical analysis.

“Using granular level data and high-dimensional fixed-effects difference-in-differences and triple-difference specifications, the baseline estimates show that sanctioned loan amounts increased by 23% in districts where SVAMITVA were implemented after rollout. The gains are distributionally progressive: borrowers from backward classes experience an additional 21% increase, while borrowers in Aspirational Districts record an additional 23% increase,” the report says.

This rise is rooted in a well-established economic mechanism. Formal property rights reduce information asymmetry, lower verification costs, and enhance lender confidence. Once ownership is clearly documented, the perceived risk of lending declines, making it easier for banks to extend credit.

At the same time, borrower behaviour evolves. Households that previously viewed their homes as static assets begin to see them as financial instruments. This shift encourages them to seek loans for housing improvement, small businesses, or non-farm enterprises, thereby diversifying rural income sources.

The report also highlights that the use of advanced econometric methods, such as high-dimensional fixed effects (HDFEs) and triple-difference estimation, strengthens the credibility of these findings. By comparing treated and control districts over time, the analysis isolates the causal impact of the scheme, reinforcing the conclusion that SVAMITVA is directly responsible for the observed credit expansion.

[HDFE models handle datasets with a massive number of categories (e.g., thousands of firms or individuals) by controlling for unobserved heterogeneity, often exceeding computational limits of standard regression. Triple-difference (DDD) estimation compares the difference-in-differences (treatment vs. control over time) between two different groups, such as a targeted group and an unaffected group.]

The combined effect is a deepening of financial inclusion. Credit flows increase not just in volume but also in reach, drawing more households into the formal financial system and reducing reliance on informal lenders.

Case for Urban Expansion

What sets SVAMITVA apart is the nature of its impact. The benefits are not evenly distributed; they are concentrated among those who were previously most constrained. The reform has had its strongest effect on marginalised groups, highlighting its role as an equalising force in credit markets.

“Among women, the strongest gains are concentrated at the bottom of the pyramid: the bottom 20% of women borrowers see a 24% increase in sanctioned loan amounts. In particular, across all such women, Muslim women exhibit an incremental 5.8% increase over the common treatment effect of 23%,” says the report.

These outcomes underline a critical insight: documentation is not merely administrative, it is transformative. By standardising property records, the scheme reduces long-standing barriers linked to caste, gender and geography, enabling broader participation in formal finance. It also strengthens women’s economic agency by creating verifiable ownership records that can bypass traditional, male-dominated property structures.

The report’s broader conclusion reinforces this point. “Overall, the findings suggest that SVAMITVA relaxed collateral constraints, deepened formal credit access, and did so in a socially and spatially inclusive manner. We recommend that a SVAMITVA-like scheme be launched in urban India as well to integrate scattered land records across states,” it says.

This recommendation points to the next frontier, urban India. Which faces its own challenges. Fragmented records spread across municipal bodies, development authorities, and state agencies, often result in legal ambiguities and transaction inefficiencies, according to the report. A SVAMITVA-like initiative could bring coherence to these systems, making land markets more transparent and easier to navigate.

Such reform could also have significant economic spill-overs. Improved land records would facilitate smoother land aggregation, reduce disputes and enable businesses to acquire contiguous parcels without excessive regulatory hurdles. For households, particularly in informal settlements, it could unlock access to formal credit in ways similar to rural areas.