New Delhi: India’s retail story is no longer a linear march from kirana counters to gleaming malls and online marketplaces. Instead, it is fragmenting, recombining and accelerating into something far more complex, and far more interesting.

Grand Thornton Bharat’s latest report, titled Inside India’s Retail Reset: The Evolution of Neighbourhood Commerce, captures this moment with unusual clarity: a system in transition, where speed, trust, access and aspiration are colliding to reshape the world’s fastest-growing consumption market. At its core, the report argues that India has entered “a decade of structural transition, shaped by rising digital adoption, shifting consumer expectations, and the emergence of new channel economics.” What is emerging is not disruption in the classic sense of one format replacing another, but something subtler and more powerful: convergence.

The macro underpinnings of this retail reset are striking. India’s digital economy is projected to reach nearly 20% of Gross Value Added (GVA measures the value of goods and services produced in an area, industry or sector, calculated as total output minus intermediate consumption) by 2029-30, up from roughly 11-12% in FY23. This is not merely an incremental shift; it is a structural reorientation of how consumption is discovered, financed and fulfilled.

Public digital infrastructure is at the heart of this transformation. With more than 450 million UPI transactions processed daily, digital payments have penetrated even the smallest retail nodes, reshaping working capital cycles for kiranas and simplifying consumer transactions. Layered on top are Aadhaar-enabled onboarding, simplified KYC norms, and a surge in merchant tech adoption, collectively lowering the barriers to entry for millions of small retailers.

Simultaneously, physical infrastructure has scaled rapidly. India’s national highway network now exceeds 1.5 lakh km, expanding at 12-13 km per day, while warehousing capacity has deepened significantly. The result is a retail backbone capable of supporting everything from neighbourhood kiranas to hyper-local dark stores.

Taken together, these developments are accelerating what the report describes as “hybrid commerce models that blend neighbourhood trust with digital convenience”.

Rise of ‘Portfolio Shopper’

Perhaps the most defining shift lies in consumer behaviour. The GTBharat report is unequivocal: “Indian consumers are no longer defined by where they shop but by why they shop”.

Drawing on insights from over 1,600 consumers across India, the study conducted by the professional services firm shows that shopping has become mission-led. Consumers now assemble a personalised “shopping portfolio”, switching seamlessly between kiranas, modern retail, e-commerce and quick commerce depending on urgency, assortment and value.

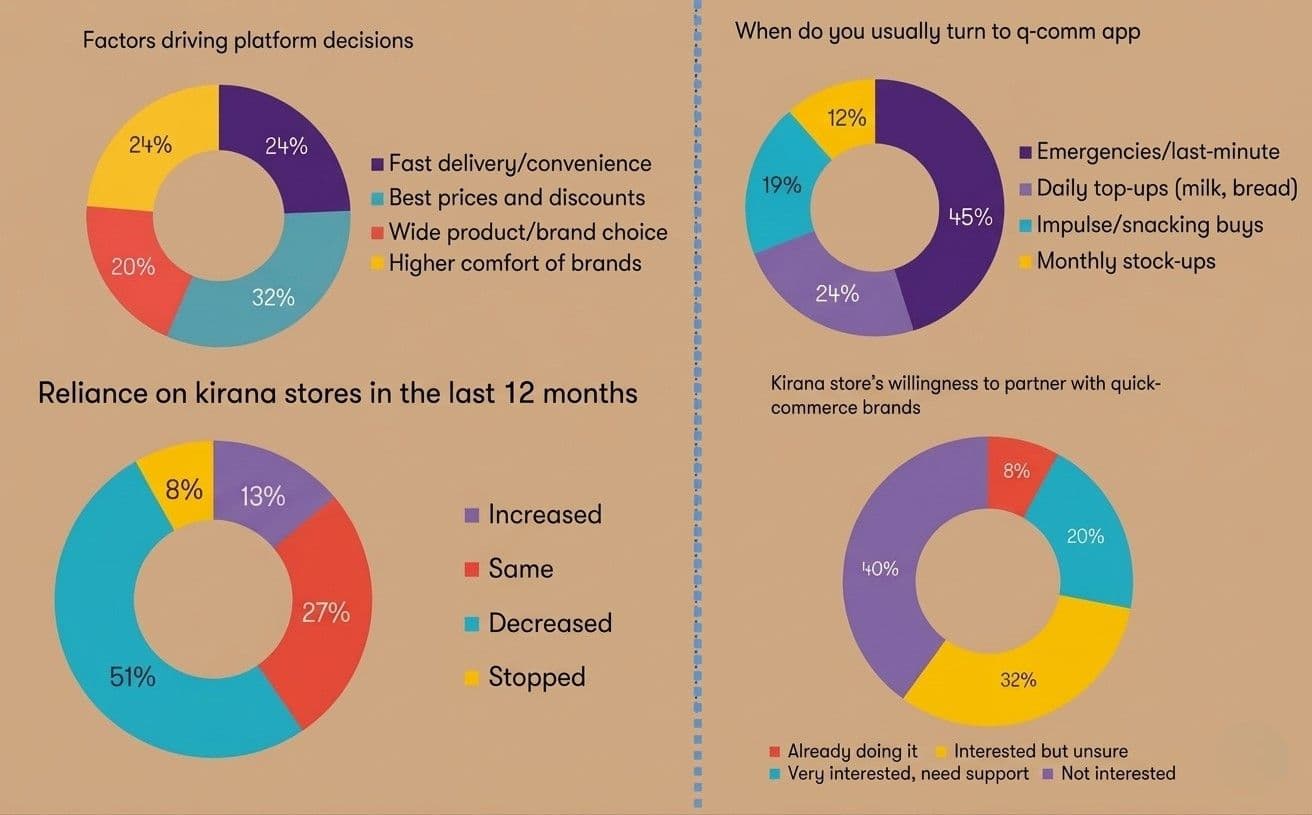

Convenience has emerged as the primary driver. When asked what matters most, respondents ranked delivery convenience above price and assortment. This is a critical behavioural shift. While discounts still matter, they are no longer the decisive factor. In fact, more than 70% of consumers said they would continue using quick commerce even if discounts were reduced.

This marks a transition from price sensitivity to time sensitivity.

Quick commerce, in particular, is carving out a distinct role. About 45% of users rely on it for last-minute or daily top-ups, while 19% use it for impulse purchases such as snacks. These are missions traditionally served by kiranas, but assured delivery timelines are gradually shifting some of this demand online.

The broader pattern is clear, as the report notes: “Consumers are not abandoning one format for another; they are layering channels based on mission relevance.”

Kiranas: Resilient, but Under Strain

Despite the digital surge, kirana stores remain the backbone of Indian retail. They continue to dominate FMCG distribution, particularly in non-metro markets, anchored in trust, proximity and flexible credit.

Yet the pressure is unmistakable. A survey of more than 1,000 kirana retailers reveals a sector that is “resilient but increasingly constrained”. Rising consumer expectations, price transparency driven by digital platforms, and the shift toward smaller, more frequent purchases are reshaping the operating environment.

Consumer data underscores this redistribution of roles. While 14% of respondents reported increased preference for kiranas over the past year and 27% saw no change, nearly half indicated a decline. But this is not a story of decline so much as repositioning. Kiranas continue to dominate planned purchases, routine grocery buying, and trust-based transactions. Their challenge lies elsewhere. Margins are tightening, credit cycles remain short, and participation in premium categories is limited by inventory risks and capital constraints. Premium stock keeping units (SKUs, popularly called barcodes, are unique, alphanumeric code assigned by retailers to identify and track specific products) often come with lower margins and higher perishability, discouraging experimentation.

Digital adoption, too, remains uneven. While UPI penetration is near universal, advanced tools such as inventory systems, POS software and digital order management are still underutilised, constrained by cost, complexity and lack of training.

And yet, there is willingness. Many kiranas are open to adopting technology, provided it is affordable, intuitive and tailored to their workflows. This presents a significant opportunity for fintechs, FMCG companies and digital platforms.

Quick Commerce: Speed is Strategic Lever

If kiranas embody continuity, quick commerce represents disruption. Not by replacing existing channels, but by redefining expectations. The report describes it as “one of the most disruptive layers in India’s retail… because it rewires how consumers think about time, immediacy, and access”.

Unlike traditional e-commerce, quick commerce operates through curated inventories housed in dark stores, typically stocking a few thousand high-velocity SKUs. In dense urban clusters, larger nodes can scale to tens of thousands of SKUs, with mega-pod facilities exceeding 50,000 items.

This model prioritises velocity over variety. High-frequency essentials dominate, but the channel is also driving rapid trial in emerging categories such as personal care minis, functional beverages and beauty accessories.

Its influence extends beyond transactions.

Quick commerce is shaping consumption patterns, compressing decision cycles and influencing how brands design SKUs. Smaller pack sizes, impulse-friendly formats and trial-oriented products are increasingly being developed with this channel in mind.

Crucially, it is also resetting benchmarks across the ecosystem. Convenience is no longer defined by proximity, but by “prompt, predictable, and frictionless” delivery.

Tier II: Next Battleground

While metros remain the epicentre of innovation, the report identifies Tier II and peri-urban markets as the next frontier of growth.

These markets are characterised by a unique tension: aspirations are rising faster than infrastructure. Consumers are digitally exposed, aspirational and increasingly premium-oriented, but local retail ecosystems often lag behind.

This creates a hybrid model. Kiranas continue to anchor daily consumption, but digital discovery drives demand for products that may not be locally available. “Digital discovery often outpaces physical fulfilment,” the report notes.

Quick commerce, even with limited penetration, plays a disproportionate role as an “expectation shaper”. It influences consumer perceptions around availability, speed and assortment, even in markets where its operational footprint is still nascent.

For kiranas, this translates into new pressures, and new opportunities too. Many are exploring WhatsApp-led commerce, home delivery and curated assortments to bridge the gap between aspiration and access.

For quick commerce players, the challenge is economic viability. Lower population density and dispersed demand increase cost-to-serve, necessitating adapted models such as smaller dark stores, hybrid delivery fleets and partnerships with local retailers.

Economics of Co-existence

Perhaps the most critical insight of the GTBharat Report lies in its analysis of channel economics. The future of Indian retail, it argues, will be determined not by which channel grows fastest, but by how value is distributed across them.

Each format operates on a distinct economic logic. Kiranas are the most cost-efficient, leveraging low rents and minimal labour. Modern retail incurs higher fixed costs but excels in experiential selling and premiumisation. E-commerce offers depth and discovery but comes with high logistics and return costs. Quick commerce, meanwhile, relies on high-frequency orders, curated assortments and monetised digital shelf space to offset last-mile costs.

This divergence is forcing manufacturers to rethink their route-to-market strategies. Increasingly, companies are deploying channel-specific SKUs, pricing architectures and promotional strategies to optimise performance across formats.

The report captures this shift as it says, “Channel economics, not channel adoption, will determine the next decade of retail growth.”

System in Convergence

What emerges from the report is a portrait of a retail ecosystem in flux but not in conflict. Kiranas, modern trade, e-commerce and quick commerce are not replacing each other; they are co-evolving.

“India's retail transformation is not about one channel overtaking another, but about deeper integration,” the report notes, adding that success will depend on “building inclusive, responsive, and economically sustainable retail ecosystems”.

This integration is already visible. Consumers move fluidly between channels. Manufacturers design portfolios across formats. Retailers experiment with hybrid models. And digital infrastructure connects it all.

The implications are profound. Retail in India is no longer about stores or platforms; it is about missions, moments and micro-markets. It is about serving a consumer who is at once value-conscious and time-sensitive, rooted in neighbourhood trust yet shaped by digital exposure.

“The next phase of retail will be defined by connected, mission-led ecosystems where kiranas remain integral to distribution but must evolve alongside modern trade and digital platforms. To stay competitive, kiranas will need to accelerate tech adoption and participate more actively in premiumisation, while larger players drive precision in forecasting, assortment, and pricing,” said Naveen Malpani, Partner and Consumer & Retail Industry Leader, Grant Thornton Bharat.

For businesses, the challenge is not choosing the right channel, but orchestrating across all of them. For policymakers, it is ensuring that this transition remains inclusive, particularly for the millions of kiranas that still anchor the system.

And for consumers, it means something simple but transformative: the freedom to shop not just where they want, but how… and why… they want.