New Delhi: India’s deal-making landscape in Q1 2026 reflects a clear divergence between sustained transactional momentum and weakening capital intensity. While overall activity remained robust, driven by strong participation from corporates and private equity, aggregate deal values continued their downward trajectory for the third consecutive quarter.

This imbalance underscores a structural shift in market behaviour, where investors and strategic players are increasingly favouring smaller, incremental transactions over large, high-risk bets amid persistent global uncertainties, mainly caused by the ongoing conflicts in West Asia.

Grant Thornton Bharat’s ‘Q1 Dealtracker’ report highlights that despite macroeconomic headwinds, including geopolitical tensions, currency volatility, and evolving trade dynamics, India’s underlying investment thesis remains intact. The quarter’s data points to a more cautious deployment environment, characterized by disciplined capital allocation, a decline in big-ticket deals, and a growing preference for bolt-on acquisitions and mid-market opportunities. The GTB report reveals a market that is not contracting, but recalibrating.

Volume Resilience vs Value Compression

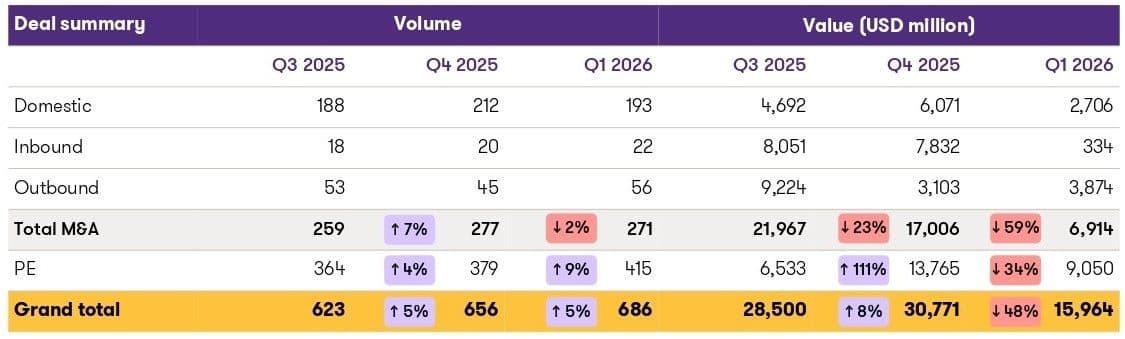

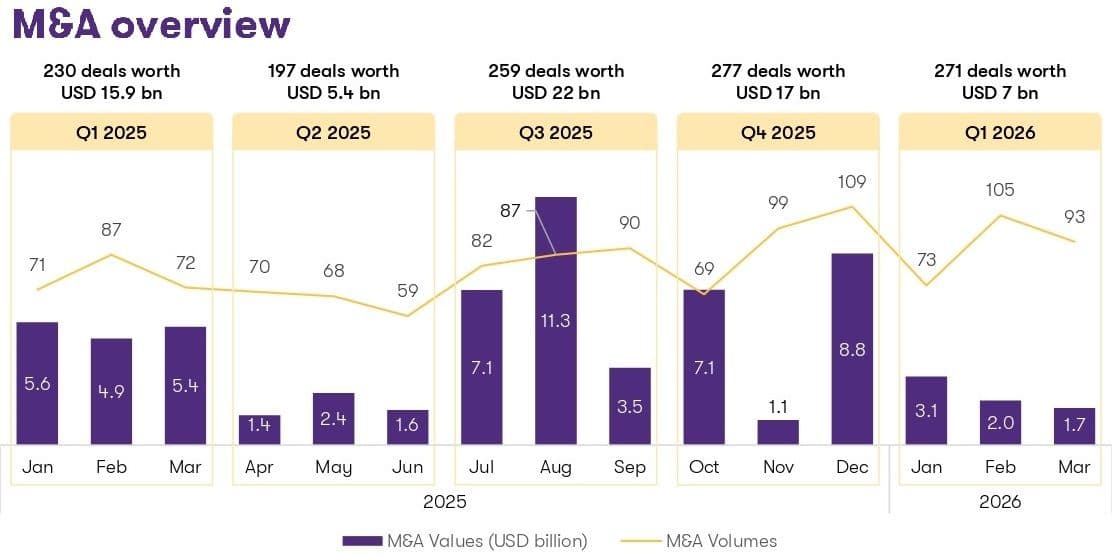

The GTB report underscores a structural imbalance in Q1 2026, with 710 deals aggregating $20 billion, marking a 5% increase in volumes, even as total values plunged 57% quarter-on-quarter. This divergence reflects a sharp decline in capital intensity, with deal-making increasingly skewed toward smaller transactions.

A key inflection point lies in the collapse of large-ticket deals. The quarter recorded just two billion-dollar deals totalling $4.1 billion, compared to seven such deals worth $15 billion in Q4 2025, while transactions above $100 million declined significantly. This has led to a sustained three-quarter downward trajectory in deal values, despite consistently high activity levels.

Shanthi Vijetha, Partner (Due Diligence), GTB, emphasizes the macro context, saying, “The quarter’s performance must be viewed in the context of persistent global headwinds, including geopolitical tensions, evolving trade and tariff environments, and currency volatility, all of which have contributed to tempered investor sentiment, particularly impacting large deals and public market activity.”

He, however, adds, “India’s deal-making environment in Q1 2026 demonstrated continued strength in activity levels. Overall, the quarter recorded 710 deals aggregating $20 billion, representing a 5% sequential increase in volumes, making it the second-highest quarterly deal volume on record after Q4 2025.”

The data suggests that while underlying economic momentum remains intact, capital deployment is becoming more selective, with investors prioritizing risk-adjusted returns over scale.

M&A Trends: Domestic Anchoring & Outbound Surge

M&A remained the core driver of activity, with 271 deals totalling $6.9 billion, making it the second-highest quarterly volume historically, yet reflecting a continued decline in value. Notably, a single outbound deal — Coforge’s $2.4 billion acquisition of Encora — accounted for 34% of total M&A value, highlighting the concentration of capital in isolated large transactions.

Domestic transactions continued to anchor the ecosystem, with 193 deals worth $2.7 billion, accounting for over 70% of volumes, but reflecting relatively modest value contributions. This indicates a strong pivot toward bolt-on acquisitions and incremental growth strategies, particularly among large corporates.

Reliance Group led activity with 10 acquisitions, followed by Marico, Gujarat Kidney and Super Speciality, and Prozone Realty with three deals each, underscoring a pattern of high-frequency, low-value strategic expansion.

Cross-border dynamics present a clear divergence. Inbound M&A declined to its lowest level since Q3 2023, reflecting subdued foreign investor sentiment, while outbound M&A surged to 56 deals worth $3.9 billion, with 24% growth in volumes and 25% growth in value.

This shift highlights India’s evolving role in global capital flows, with domestic corporates increasingly pursuing international opportunities amid favourable valuations abroad.

Divergence Between Volume and Value Leaders

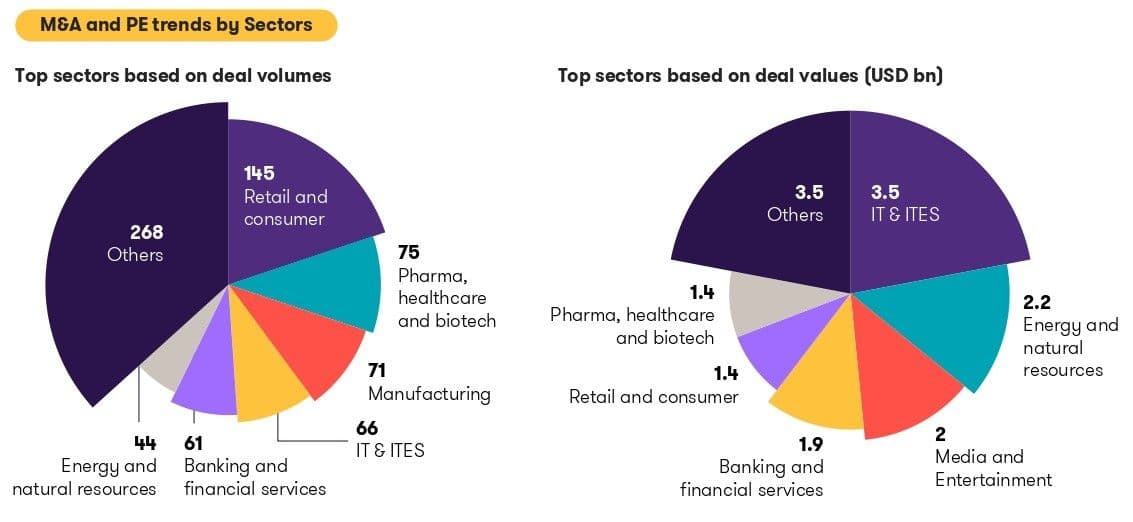

Sectoral analysis reveals a clear bifurcation between consumption-led sectors driving volumes and technology and infrastructure sectors dominating value. Retail and consumer led with 145 deals, reflecting a 20% increase in volumes, yet deal values declined 59% to $1.4 billion, primarily due to the absence of large-ticket transactions seen in prior quarters.

In contrast, IT & ITeS dominated value creation, contributing $3.5 billion across 66 deals, or over 22% of total deal value. This performance was anchored by a few marquee deals, with tech services contributing 77% of value, while startups accounted for 53% of volumes, highlighting a dual-speed ecosystem.

Energy and natural resources also demonstrated strong growth, with 44 deals totalling $2.2 billion, reflecting 22% growth in volume and 31% growth in value, driven by sustained investments in renewables and power generation.

The media and entertainment sector recorded $2 billion across 23 deals, with 87% of value driven by a single sports transaction, reinforcing the increasing institutionalization of sports assets.

Pharma, healthcare and biotech remained active with 75 deals totalling $1.4 billion, though values declined 34%, reflecting a drop in average deal size from $30 million to $18.3 million. HealthTech led both volumes and value, signalling continued digital transformation.

Meanwhile, BFSI experienced a sharp contraction, with 61 deals worth $1.9 billion, reflecting a 25% decline in volumes and an 85% decline in value, primarily due to the absence of large deals that had previously driven sectoral performance.

Measured Capital Deployment

Private equity activity remained resilient in participation, with 415 deals totalling $9.1 billion, compared to 379 deals worth $13.8 billion in Q4 2025, indicating a moderation in value despite stable deal flow. Large deals above $100 million declined sharply in aggregate value, from $10.5 billion to $5.5 billion, reinforcing a shift toward disciplined capital deployment.

Vishal Agarwal, Partner, GTB, highlighted this recalibration, saying, “Private equity activity in Q1 2026 moderated following a strong close to 2025. The softer start to the year suggests a degree of recalibration in deployment pace, potentially reflecting evolving global conditions, including ongoing geopolitical developments that may be influencing investor timing and risk appetite.”

Despite this moderation, investor confidence in high-growth segments remains intact, as evidenced by the emergence of three new unicorns during the quarter.

“From a sectoral standpoint, media and entertainment emerged as the top sector by value ($1.8 billion) in Q1 2026... Excluding this outlier, sectoral activity remained more aligned with recent trends,” said Agarwal.

“Overall, Q1 2026 indicates a continuation of the measured investment approach seen in recent quarters, with investors maintaining a balanced stance between deployment discipline and sector diversification while remaining attentive to evolving market,” he said.

Public market activity, however, weakened significantly, with IPOs and QIPs declining sharply due to volatility, reinforcing the growing reliance on private capital.

On the broader outlook, Vijetha says, “While global headwinds have impacted large deal activity and capital markets, however India’s underlying investment narrative remains intact… The sustained deal volumes, strong private equity participation, and record outbound activity reinforce confidence in the market, with deal-making expected to remain resilient through 2026, albeit risk appetite for large deals may be tempered.”

(Cover photo by Amina Atar on Unsplash)